Tax preparation rarely happens in isolation. In most accounting firms, multiple professionals contribute to a single return—entering data, reviewing calculations, or handling specific sections of the filing. This raises a practical question that is often overlooked: how are multiple contributors formally recorded in a tax return?

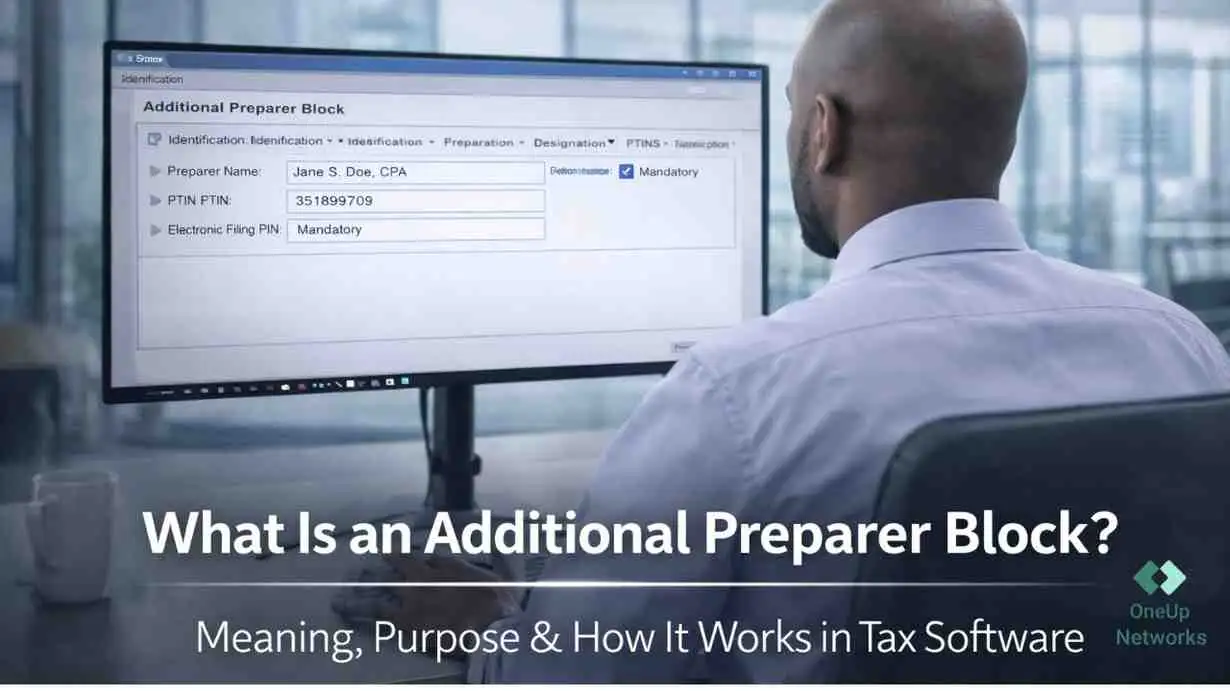

The answer lies in what tax software refers to as an additional preparer block. Understanding this concept is not only about compliance—it is about accountability, workflow clarity, and audit readiness in modern tax environments. An additional preparer block is a section within a tax return that records the details of professionals who contributed to the return but are not the primary signing preparer.

What Is an Additional Preparer Block?

An additional preparer block captures information about one or more contributors involved in preparing a tax return alongside the primary preparer. In standard filing structures, a primary preparer signs the return and assumes formal responsibility. In practice, however, preparation is distributed across teams. The additional preparer block reflects that operational reality by ensuring that contributions are visible and traceable rather than implied. Instead of presenting a return as the work of a single individual, it recognizes the collaborative nature of modern tax preparation.

Why Does This Block Exist?

The purpose of this block is not administrative—it is structural.

In multi-user environments, several gaps emerge without proper attribution:

- who handled specific sections of the return

- who made key adjustments or corrections

- who reviewed or validated calculations

- who should be contacted if questions arise later

The additional preparer block introduces traceability into the preparation process and links work to individuals.

This becomes particularly important in firms where:

- returns move through multiple review levels

- teams operate across locations

- deadlines require parallel work streams

Without structured attribution, responsibility becomes unclear—and that affects both workflow efficiency and oversight.

What Information Does It Typically Include?

While formats vary across software, the additional preparer block generally records:

- preparer name

- firm or organization name

- identification number (such as PTIN, where applicable)

- role or level of involvement (in some systems)

In many tax software environments used by accounting firms, these fields are either manually maintained or linked to user profiles within the system. This information may not always be client-facing, but it remains part of the internal and compliance record. Its purpose is not visibility—it is accountability.

How It Works in Practice

In most tax software environments, the additional preparer block is populated as multiple users interact with a return.

A typical workflow looks like this:

- a junior preparer enters initial data

- a senior accountant reviews calculations

- a manager adjusts or finalizes entries

- a partner signs the return

Only one individual is designated as the signing preparer. However, the additional preparer block captures the involvement of others, creating a layered record rather than a single-point attribution. This reflects how work actually happens inside firms—not how it appears on the final signature.

Where It Becomes Important

The additional preparer block becomes critical when traceability is required.

This includes:

- large or complex returns

- firms with multiple contributors per engagement

- structured review environments

- audits or compliance checks

In these situations, identifying who worked on what is not optional—it is necessary for verification, accountability, and internal control.

Common Misunderstanding

A frequent assumption is that anyone who works on a return is automatically recorded. In practice, this is not always the case.

In many systems, additional preparer details must be:

- explicitly entered

- configured through system settings

- or tracked through workflow tools

If this process is not followed consistently, contributions may not be formally documented. The block exists—but its accuracy depends on how the system is used.

Additional Preparer Block vs Primary Preparer

This distinction is essential for understanding responsibility.

| Role | Responsibility |

|---|---|

| Primary Preparer | Signs the return and holds formal responsibility |

| Additional Preparer | Contributes to preparation but does not sign |

The primary preparer is legally accountable for the return. Additional preparers are operationally involved but are not the final authority.

Where Friction Happens in Real Firms

The concept is straightforward, but implementation is often inconsistent.

Common issues include:

- multiple users working without consistent attribution

- lack of a standard process for recording contributors

- uncertainty about who should be listed

- incomplete or inconsistent preparer information

These are not software failures—they are workflow gaps. The additional preparer block only works when firms use it deliberately and consistently.

When It Actually Becomes a Problem

In many cases, missing or incorrect preparer attribution goes unnoticed—until it becomes relevant.

For example:

- during an audit, firms may struggle to identify who made specific changes

- internal reviews may lack clarity on responsibility for adjustments

- compliance checks may reveal incomplete preparer records

- accountability becomes difficult when multiple users were involved

At that point, the issue is no longer administrative—it affects audit readiness and internal control. The absence of clear attribution turns routine questions into time-consuming investigations.

When Attribution Becomes Unclear

In some situations, multiple preparers may work on a return without clearly defined roles.

For example:

- one user updates figures after review without documentation

- multiple revisions occur without tracking ownership

- responsibility shifts during tight deadlines

In these cases, the return may still be technically correct, but identifying who made specific decisions becomes difficult. The risk is not in the numbers—it is in the ability to explain how those numbers were produced.

Example Scenario

Consider a mid-sized firm preparing a corporate return:

- a staff accountant completes data entry

- a senior makes adjustments

- a manager performs final review

- a partner signs the return

Without structured attribution:

- contributions remain informal

- responsibility is assumed rather than recorded

With proper use of the additional preparer block:

- each contributor is documented

- responsibility becomes traceable

The difference is not visible to the client, but it directly affects internal clarity and audit readiness.

How This Fits into Modern Tax Workflows

Tax preparation in 2026 is increasingly:

- collaborative

- system-driven

- distributed across teams

As a result, firms are placing greater emphasis on:

- workflow tracking

- user-level activity logs

- structured attribution

The additional preparer block is one part of this broader shift toward transparency and accountability in preparation processes.

When Firms Should Pay Attention to This

In smaller firms where a single preparer handles a return, the additional preparer block may not always be necessary. However, once multiple individuals contribute—even informally—the absence of structured attribution can create gaps that are difficult to address later.

In practice, many firms follow simple internal rules:

- if more than one person edits a return, contribution should be recorded

- if a review materially changes calculations, attribution should be clear

- if a return passes through multiple levels, involvement should be traceable

These are not always formal requirements, but they reflect how experienced teams maintain clarity and accountability. The goal is not to document everything—it is to document what matters when questions arise.

Frequently Asked Questions

A section that records contributors to a tax return who are not the primary signing preparer.

A section that records contributors to a tax return who are not the primary signing preparer.

Not always. It depends on workflow, software configuration, and the number of contributors.

Typically no. These details are part of internal or compliance records.

Final Perspective

The additional preparer block reflects a simple reality: modern tax preparation is rarely the work of one individual. As workflows become more collaborative and structured, accurately capturing contribution becomes part of operational discipline—not just documentation. It ensures that responsibility, contribution, and accountability remain aligned within the systems firms rely on every day.

Struggling to Track Multi-User Contributions in Tax Workflows?

As tax preparation becomes more collaborative, maintaining clear attribution and accountability across multiple preparers becomes increasingly complex. OneUp Networks helps firms operate in structured, secure environments where user activity, access, and workflow visibility remain consistent and controlled.

- Book a Demo – See how tax software runs in a controlled multi-user environment with clear user-level tracking.

- Request a Quote– Test workflow visibility, system performance, and secure access across your team.

- Request a Quote – Get a tailored setup based on your firm’s size, workflow structure, and software requirements.

You May Also Like These Articles:

- Facing Issues with Drake Tax Desktop Software? Find Answers To FAQs & Cloud Hosting Solutions

- Data Protection in the Cloud: How to Safely Host Tax Applications?

- Sign Up Form

- What Is an Electronic Return Originator (ERO)? A Simple Guide for Tax Professionals

- What Is IRS Form 1040 Schedule 2? Who Needs to File It and How to Complete It (2025 Update)